TORONTO – May 04, 2020: Urbanation Inc., the leading source of information and analysis on the GTA condominium market since 1981, released its Q1-2020 condominium market results today.

New Condominium Market

In the first quarter period leading up to when strict protocols were enacted to limit the spread of the COVID-19 coronavirus, the GTA condominium market was beginning to resemble the start of the overheated conditions last seen in late 2016 and early 2017.

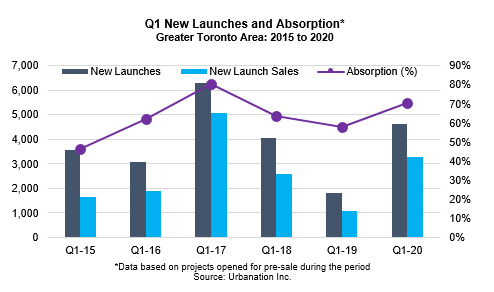

As a whole, new condominium sales recorded their second best Q1 on record with 5,626 units, rising 85% year-over-year. Developers launched 4,623 units in Q1-2020 (93% of which happened in February), 2.5 times more than a year ago (1,829 units) and the highest first quarter level of new openings outside of peak periods in 2012 and 2017 (both above 6,000 units). Absorption was exceptionally strong as 71% of the new units offered were sold by quarter-end, aided by the fact that no projects officially launched during March. In fact, only 2017 had experienced higher success rates at new openings, showing rejuvenated demand from investors before the pandemic hit. As a result, unsold inventory edged down by 1% from a year ago to 13,024 units, which was 15% below its 10-year average, with total absorption in actively marketed projects rising to 87%. Strong conditions led to accelerated annual growth in sold new condo prices of 11% in Q1-2020, which reached an average of $865 psf for units in development. Unsold prices grew by 9% annually to $1,085 psf.

Most projects in development were already under construction and not actively marketing when COVID-19 hit, with 92% of the 76,177 units under construction pre-sold. As well, the 33,261 units in pre-construction were 79% sold, meaning most projects had met their targets to obtain construction financing.

Similar to the Q1 and Q2 periods of 2009 following the onset of the Great Recession, new launches are expected to become very limited over the next six months, which should help keep absorption levels high and inventories low.

Industry Survey

Overall, the industry was cautiously optimistic regarding the near-term prospects for the condominium market. According to the results of Urbanation’s survey of market expectations conducted during the last two weeks of April, which included responses from about 100 representatives of the new condominium development industry, more than half of the projects that were planned to launch this spring are currently being delayed only until the fall of this year, with the bulk of the remaining projects expected to come to market in the winter or early spring of next year. As well, close to half of respondents expected that pricing will hold steady for new condo launches this year relative to achieved prices in projects launched in late 2019 and early 2020, albeit with a small increase in buyer incentives and a more moderate level of absorption. This was closely followed by a 40% share expecting a slight decline in pricing with a large increase in incentives and a low-to-moderate pace of absorption. Few expected a large decline in prices but even fewer expected a rise in prices, illustrating that developers will likely take a cautious approach to reintroducing projects to the market this year.

Resale Market

To illustrate how quickly the condo market changed as a result of COVID-19, resale activity was up 25% year-over-year during the first half of March 2020 and fell 21% year-over-year in the second half of the month, with even steeper annual declines of over 70% reported for April. However, the GTA market was exceptionally tight leading into the COVID-19 period, creating spillover demand that has enabled the limited number of units on the market to continue transacting. In fact, the average sale price-to-list-price ratio has remained near 100% through April, and the average days on market was unchanged at 18 days.

Nonetheless, as sales have declined by a much faster pace than new listings, resale condo prices have experienced some reduction. Preliminary resale data for April reported a 2.2% annual decline in average resale prices for condos. However, median prices remained 4.7% higher than a year ago, indicating that most of the decline has occurred for higher-priced units.

Overall, most participants of the industry survey felt resale values would be down by about 5% at the end of 2020 compared to the end of 2019.

Completions and Investor Supply

It will be particularly important in the coming months to monitor investor listings for downside risks to condo prices, as some may feel it will be an opportune time to sell once physical distancing restrictions are relaxed and the market begins to function more normally. With the exceptionally strong growth in prices and equity accumulation realized in recent years, stretched finances and a softer rental market may create a stronger desire to “cash out”. This could be further enhanced by listings from former Airbnb hosts no longer able to operate their business, and assignment listings from units reaching occupancy.

Heading into COVID-19, close to 29,000 new condominiums were scheduled for occupancy in 2020 in the GTA, which would have been almost 40% higher than the previous high set in 2014 at just over 21,000 units. As a result of the delays being experienced at construction sites, the schedule has been revised down to approximately 25,000 units. As some revised timelines are probably still too optimistic given that sites will have to continue adhering to safety protocols that will limit productivity, and supply chain disruptions will persist for some time, a more realistic estimate at this time may be 20,000 units. This considers that over 7,000 units already reached occupancy in the first quarter and another 13,500 are currently slated by the end of the third quarter. With deliveries expected to rise by at least 38% from 2019 (14,500), and more than half of units pre-sold to investors, supply will grow this year. As most investors tend to offer their units for rent upon completion, the growth in supply should result in a decline in rents, particularly in light of reduced population growth and projected job losses. April data for the condo rental market showed lease activity down 71% year-over-year, with new listings almost holding equal to last year (-0.9%) and average rents declining 1.2% to $2,342.

ABOUT THE CONDOMINIUM MARKET SURVEY

Urbanation has been surveying the GTA condominium market each quarter since 1981 through established relationships with the region's developers, brokerages, and lenders. In addition, our team of highly skilled researchers conduct regular site visitations to compile the industry's most in-depth coverage on every new project in development across the region.

Urbanation's Condominium Market Survey subscription provides access to our historical online database of new condominium developments in the GTA and Hamilton-Grimsby, including full project profiles and unit information, and market reporting metrics such as sales totals, absorption rates, inventory levels, average sold and unsold prices per sf, incentives, and more. Data is reported at the individual project level, with tools to generate regional, municipal, and submarket totals. Information on upcoming new condo project launches and future developments are tracked in our proposed database, which is also included as part of the Condo Market Survey subscription.

ABOUT URBANATION

Urbanation is a real estate consulting firm that has been providing market research, in-depth market analysis and consulting services to the apartment industry since 1981. Urbanation uses a multi-disciplinary approach that combines empirical research techniques with first-hand observations and site visits. Urbanation offers subscription services and custom market studies covering the new construction condominium and purpose-built rental apartment markets in the Greater Toronto Area.

www.urbanation.ca Contact: Shaun Hildebrand

www.twitter.com/urbanation [email protected]

Latest Research

February 9, 2026

GTA Land Transaction Volume Down 20% in 2025February 9, 2026

Rental Vacancy in Ottawa Increased to 3.5% in Q4January 29, 2026

Nearly 10,000 GTHA Rentals Started Contruction in 2025January 21, 2026

New Condo Sales Fall for 4th Year to Lowest Since 1991November 4, 2025

Ottawa Rental Starts Reach Multi-Decade High in Q3October 28, 2025

GTHA Rental Projects Forge Ahead in Q3 Despite Declining Rents

In The News

March 18, 2026

Public-private partnership launches $1.3-billion fund to purchase unsold GTA condosFebruary 9, 2026

Condo crash pushes down Toronto asking rents to $2,500 a month due to ‘sheer volume of supply’February 3, 2026

Toronto is a renter's market — for now — as record glut of condos and apartments collideFebruary 2, 2026

Rental construction surged in Q4-2025January 23, 2026

“No New Condo Completions” In GTHA By Decade’s End: UrbanationJanuary 23, 2026

Toronto and Hamilton-area new condo sales in 2025 were the lowest in 35 years, says Urbanation