TORONTO – July 15, 2020: Urbanation Inc., the leading source of information and analysis on the GTA condominium and rental apartment markets since 1981, released its Q2-2020 rental market results today.

Vacancy Rate Increases to 1.8% as Rental Construction Remains Near 40-year High

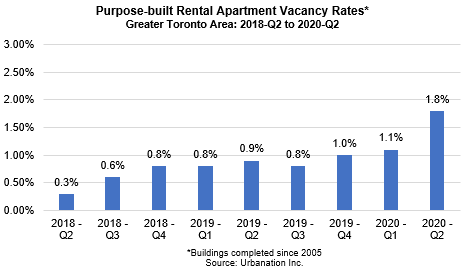

Urbanation’s survey of purpose-built rental apartment projects that have been completed in the GTA since 2005 reported a vacancy rate of 1.8% in Q2-2020, rising from 1.1% in Q1-2020 and 0.9% a year ago in Q2-2019. The availability rate, which measures vacant units as well as units where the tenant has provided notice to vacate, rose to 3.2% (2.3% in Q1-2020 and 2.0% in Q2-2019). Both the vacancy and availability rate reached their highest levels since Urbanation began surveying the data in Q1-2015.

Vacancy rates were highest in the former City of Toronto (largely representing the Toronto core) at 2.3%, compared to 2.0% in the outer 416 regions of Etobicoke, North York and Scarborough, and 0.9% in the 905 region.

Within buildings that have been completed for at least one year, average monthly rents for units that became available during the second quarter declined by 3.7% year-over-year to $2,420, based on an average unit size of 751 sf. However, when measured on a per square foot (psf) basis, rents declined by only 0.6% from last year to $3.22 psf. The decline in rents was additional to incentives being offered. Urbanation found that 31 out of 73 surveyed buildings offered some form of incentive to attract renters, with the most common being one month of free rent.

At the end of Q2-2020, the number of purpose-built rentals under construction in the GTA totaled 13,358 units, remaining near its more than 40-year high reached in the previous quarter (13,580) and 17% higher than a year ago in Q2-2019 (11,421 units). Close to two-thirds of rentals under construction were located in the former City of Toronto.

Declines in Condominium Rents Focused within Downtown Markets

Total condominium apartment lease activity for unfurnished, long-term rentals in registered buildings declined 31% year-over-year in Q2-2020 to 6,114 units. However, by June as the GTA was entering into stage 2 of the province’s economic reopening plan, lease activity during the month rebounded by 79% from the April low to come within 5% of its year ago level in June 2019.

At the same time that demand for rentals declined in the second quarter as a result of COVID-19, condo rental supply surged to record highs. The total number of listings during the second quarter increased 22% year-over-year to 13,576 units, while active listings still available at the end of June more than tripled from a year ago to 6,757 units. Measured against lease activity in Q2, the remaining inventory equaled 3.3 months of supply, which compared to less than one month of supply last year.

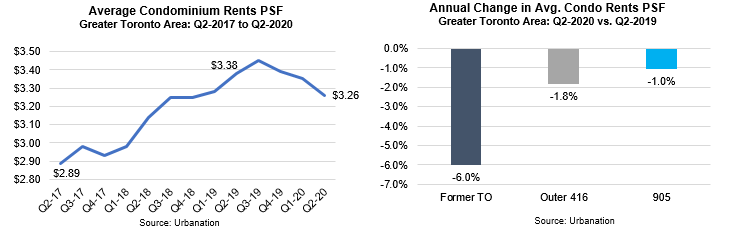

The softening in the condo rental market led rents to decline by 3.6% year-over-year to $3.26 psf ($2,356 for 722 sf). However, the decline was almost entirely concentrated in the former City of Toronto, which reported a 6.0% annual decrease to $3.59 psf ($2,453 for 683 sf). In the outer 416 region, rents were down by 1.8% from a year ago to $3.02 psf ($2,285 for 756 sf), while in the 905 region rents held up best with a 1.0% year-over-year decline to $2.78 psf ($2,181 for 786 sf). The stronger rent decline in the former City of Toronto may be attributable to relatively less demand for more expensive rentals given the economic hardship and the expectation that work from home arrangements may become permanent, a drop in foreign students, as well as a greater concentration of supply in the core due to rising condo completions and units formerly offered as short-term rentals.

One indicator of the conversion of short-term rentals to long-term rentals is the number of furnished condo rental listings offered for 12 month leases, which grew 52% in Q2-2020 to 1,877 units, representing 12% of all condo rental listings in the GTA during the quarter and 21% of the growth in total condo rental listings compared to last year. With demand for furnished long-term rentals declining in Q2-2020 (lease activity fell 24% year-over-year), average monthly rents for furnished units dropped 12.5% from last year to $2,492.

“The GTA rental market has been clearly impacted by COVID-19, though the transition has been orderly so far with vacancy remaining low and rent declines being modest outside of some specific pockets in the city. Government income support has played a big role as job losses mounted and immigration dropped”

- Shaun Hildebrand, President of Urbanation.

ABOUT URBANRENTAL

Urbanation’s UrbanRental subscription provides quarterly market reports and online historical database access for newly completed, under construction and proposed purpose-built rentals in the GTA and Hamilton-Grimsby, in addition to secondary condominium rentals in registered buildings. Urbanation surveys purpose-built rental projects developed since 2005 for market rents and vacancies through our direct relationships with rental management companies, and our continuous monitoring of information on units becoming available for rent. We regularly conduct in-person site visits and provide full profiles for every new rental project surveyed. Our rental database also tracks development progress for every new rental project under construction and proposed for future development.

ABOUT URBANATION

Urbanation is a real estate consulting firm that has been providing market research, in-depth market analysis and consulting services to the apartment industry since 1981. Urbanation uses a multi-disciplinary approach that combines empirical research techniques with first-hand observations and site visits. Urbanation offers subscription services and custom market studies covering the new construction condominium and purpose-built rental apartment markets in the Greater Toronto Area.

www.urbanation.ca Contact: Shaun Hildebrand

www.twitter.com/urbanation [email protected]

416 922 2200 ext. 243

Latest Research

June 23, 2026

Ontario Student Housing Deliveries Set to Reach Record in 2026May 4, 2026

Over Half of Ottawa Rental Buildings Offering IncentivesApril 26, 2026

GTHA Rental Vacancy Rises to 5.4% in Q1April 16, 2026

Standing Condo Inventory Hits Record High in Q1February 9, 2026

GTA Land Transaction Volume Down 20% in 2025February 9, 2026

Rental Vacancy in Ottawa Increased to 3.5% in Q4

In The News

April 30, 2026

Incentive offers rise as apartment operators compete with condos for tenantsApril 28, 2026

The vacancy rate is up for new Toronto area rental buildings, so why is it still so expensive to rent?April 21, 2026

Toronto's condo market 'hits bottom' with some developers looking at selling units below the cost to buildApril 17, 2026

'Somewhere to put worker bees': Why Canada's micro-condos are losing their appealApril 17, 2026

Toronto’s condo market sets a new record: zero new projects launched in the first quarterApril 10, 2026

Average national asking rents fall to $2,008 after largest drop in five years: report