TORONTO – October 16, 2020: Urbanation Inc., the leading source of information and analysis on the GTA condominium and rental apartment markets since 1981, released its Q3-2020 rental market results today.

Vacancy Rate Increases to Nearly 3% in Former City of Toronto

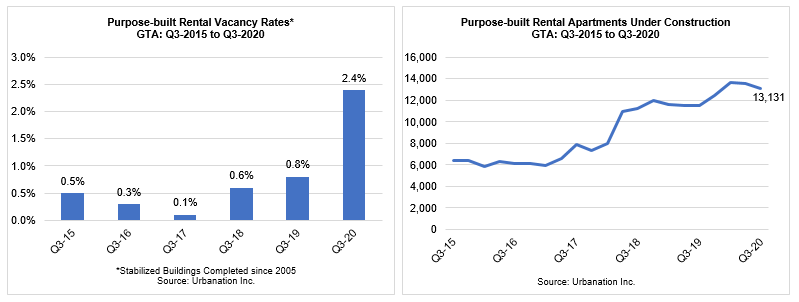

Urbanation’s survey of newer purpose-built rental apartment projects that have been completed in the GTA since 2005 reported a vacancy rate of 2.4% in Q3-2020, which was three times higher than in Q3-2019 (0.8%) and the first time vacancy rates surpassed 2% in the GTA in 10 years. Within the former City of Toronto (mainly representing the downtown and midtown markets), vacancy rates increased to 2.8% from 0.7% a year ago.

Total occupancy in newer purpose-built rental buildings across the GTA, including recently completed buildings still in their initial lease-up, remained essentially unchanged from a year ago at an average of 90%. However, within the four buildings totaling 988 units that reached completion so far in 2020, occupancy averaged 34% in Q3-2020, which compared to an average occupancy rate of 64% in Q3-2019 for the eight projects totaling 3,155 units that reached completion in the same year-to-date 2019 period.

Average monthly rents for units that became available for rent during the third quarter (within buildings that have been completed for at least one year) declined by 5.8% year-over-year to $2,373. However, some of the rent decline could be attributed to a decrease in the average available unit size to a record low 740 sf from 767 sf a year earlier, indicating that turnover has been relatively stronger for smaller units. On a per square foot basis, rents declined by 2.4% year-over-year to $3.21 psf. Within the former City of Toronto, monthly rents declined 9.3% year-over-year to $2,549 with average available unit sizes down from 716 sf in Q3-2019 to a low of 676 sf in Q3-2020. On a per square foot basis, rents in former Toronto were down 3.8% year-over-year to $3.77 psf. The reported decline in rents was additional to incentives. Urbanation found that most rental buildings surveyed were offering incentives to attract new tenants, which mainly included one month of free rent, move-in bonuses and, to a lesser extent, two months of free rent.

Purpose-built rental development remained elevated in the third quarter compared to previous years, with 13,131 units under construction, down from the recent high of 13,663 units in Q1-2020 but up from a year ago (11,522 units) and more than double the level from four years ago (6,117 units). A total of 5,276 new rental units are scheduled for completion in the GTA in 2021, the highest level in more than 25 years and up from 988 units completed in 2020.

Condo Rents Continue to Fall Despite Record Number of Lease Transactions

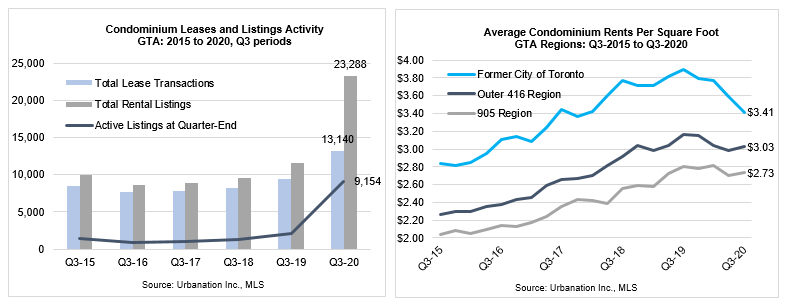

Total unfurnished, long-term condominium rental lease transaction volume in the GTA grew 39% year-over-year during the third quarter to a record high 13,140 units. Activity surged due to a doubling in the number of condo rentals listed for lease during the quarter to 23,288 units and an annual reduction in average monthly rents of 9.4% to $2,249 — the lowest rent level since Q1-2018. While there were some signs of improvement in the market in the last three months as the ratio of leases-to-listings increased to 56% from 45% in the second quarter, and the quarter-over-quarter decline in average per square foot rents slowed to 2.1% from a 2.7% decline in Q2, rents will continue to face further downward pressure due to the record amount of supply on the market. At the end of Q3, active condo rental listings totaled 9,154 units, 4.5 times higher than a year earlier.

The 7.5% year-over-year decline in average per square foot condo rents in the GTA in the third quarter to $3.19 psf was heavily weighed down by weakness in the former City of Toronto, where average per square rents fell 12.3% annually to $3.41 psf ($2,290). In the outer 416 region (Scarborough, Etobicoke, North York), the annual decline in rents was 4.5% to $3.03 psf ($2,219), while 905 region rents were down the least by 2.5% annually to $2.73 psf ($2,162). Of note, average rents increased 1.1% quarter-over-quarter in both the outer 416 and 905 regions, while continuing to fall in the former City of Toronto with an accelerated quarterly decline of 5.0%. Within the former City of Toronto, the steepest year-over-year declines in average per square foot rents were found in the East Bloor/The Village submarket near U of T and Ryerson University (-16.8%), the Downtown Core (16.0%), the Entertainment District (-15.9%), and CityPlace (-14.3%).

“The GTA rental market showed some improvement in the third quarter within more suburban areas, while experiencing weakened conditions in the downtown areas as renters reevaluated the costs of living in the central core as most offices, post-secondary schools and entertainment venues remained closed.

While it was encouraging to see the large increase in lease activity in third quarter as renters took advantage of recent discounts, the market will continue to face challenges heading into 2021 from restrained demand caused by COVID-19 and elevated supply levels”.

- Shaun Hildebrand, President of Urbanation.

www.urbanation.ca Contact: Shaun Hildebrand

www.twitter.com/urbanation [email protected]

416 922 2200

Latest Research

July 27, 2026

GTHA RENTAL MARKET SHOWS IMPROVEMENT IN Q2July 20, 2026

GTHA NEW CONDO SALES INCREASE OVER 50% IN Q2June 23, 2026

Ontario Student Housing Deliveries Set to Reach Record in 2026May 4, 2026

Over Half of Ottawa Rental Buildings Offering IncentivesApril 26, 2026

GTHA Rental Vacancy Rises to 5.4% in Q1April 16, 2026

Standing Condo Inventory Hits Record High in Q1

In The News

July 28, 2026

GTHA rental market shows improvement in Q2July 21, 2026

Bulk investor buying helps resuscitate condo purchases in the Toronto regionJuly 21, 2026

New condo sales in the GTHA were up for the first time in 3 years, but report says supply now ‘thinning quickly’April 30, 2026

Incentive offers rise as apartment operators compete with condos for tenantsApril 28, 2026

The vacancy rate is up for new Toronto area rental buildings, so why is it still so expensive to rent?April 21, 2026

Toronto's condo market 'hits bottom' with some developers looking at selling units below the cost to build