TORONTO – May 01, 2024: Urbanation Inc., the leading source of data and analysis on the GTHA condominium and rental apartment markets since 1981, released its Q1-2024 rental market results today.

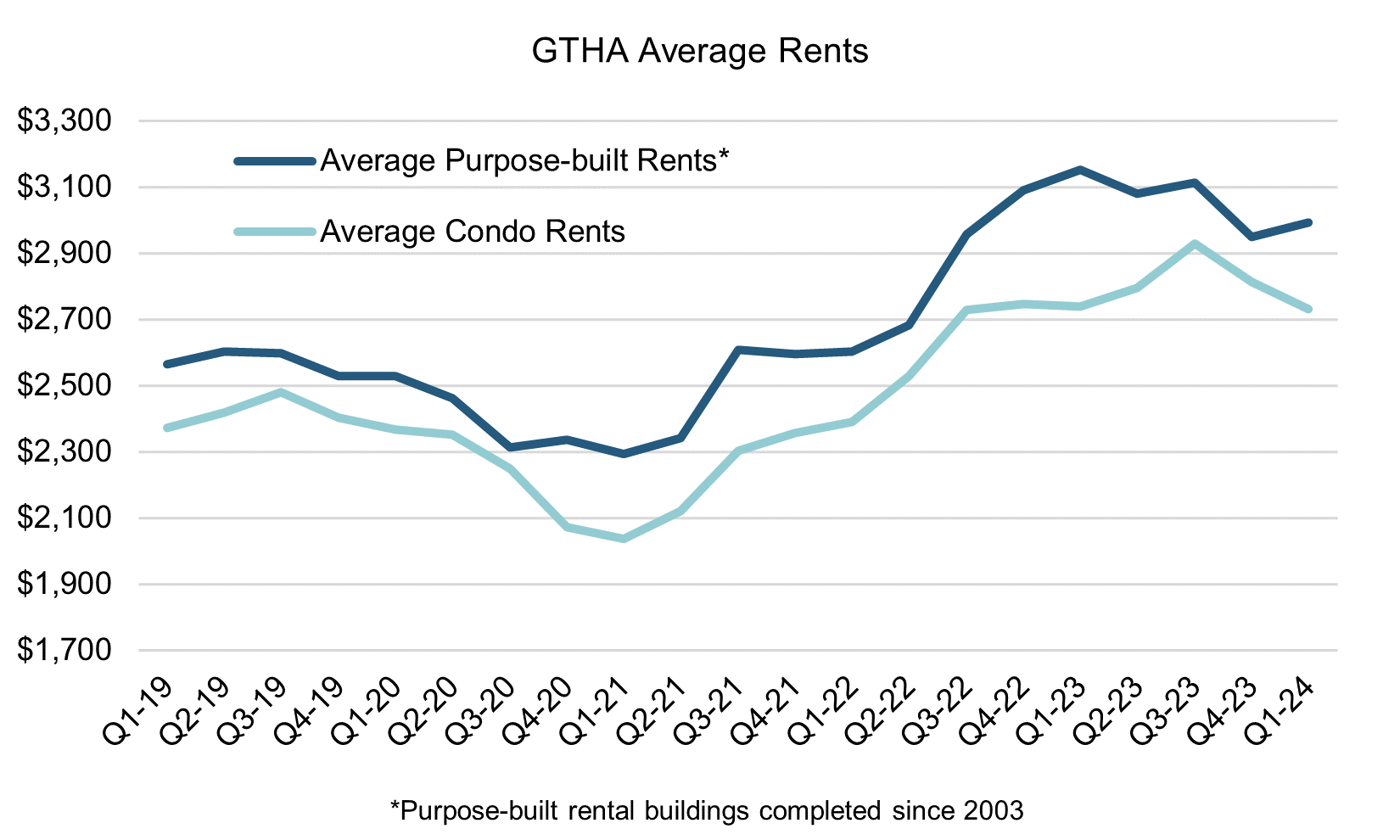

- Average condo rents declined 7% from the high in Q3-2023 to $2,732 ($3.89 per sf) in Q1-2024

- Annual condo rent growth slowed to 1.6% as condo completions reached a record high

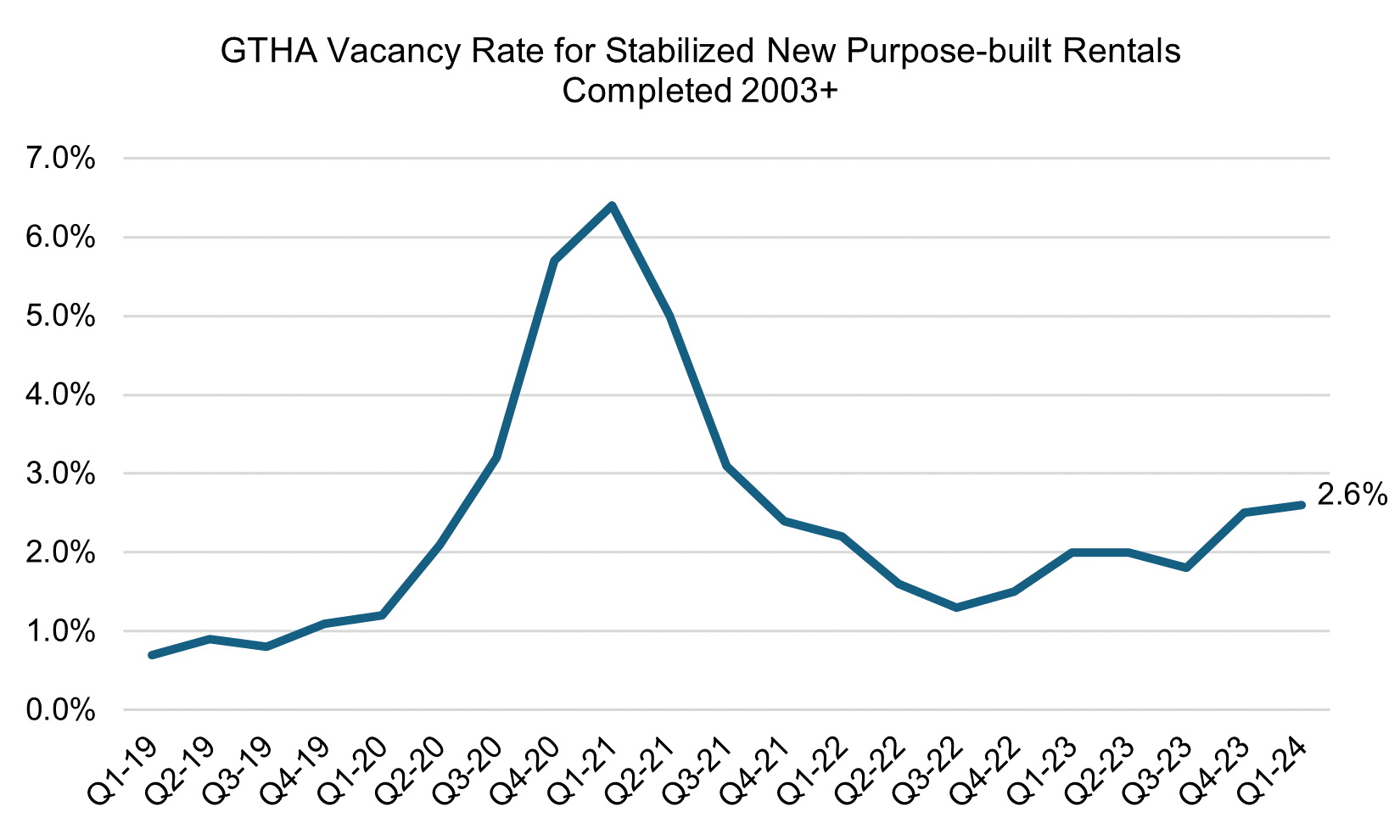

- Purpose-built rental vacancy edged up to 2.6%. Vacancy averaged 3.5% in non-rent controlled buildings compared to 1.7% in rent-controlled buildings completed before 2019

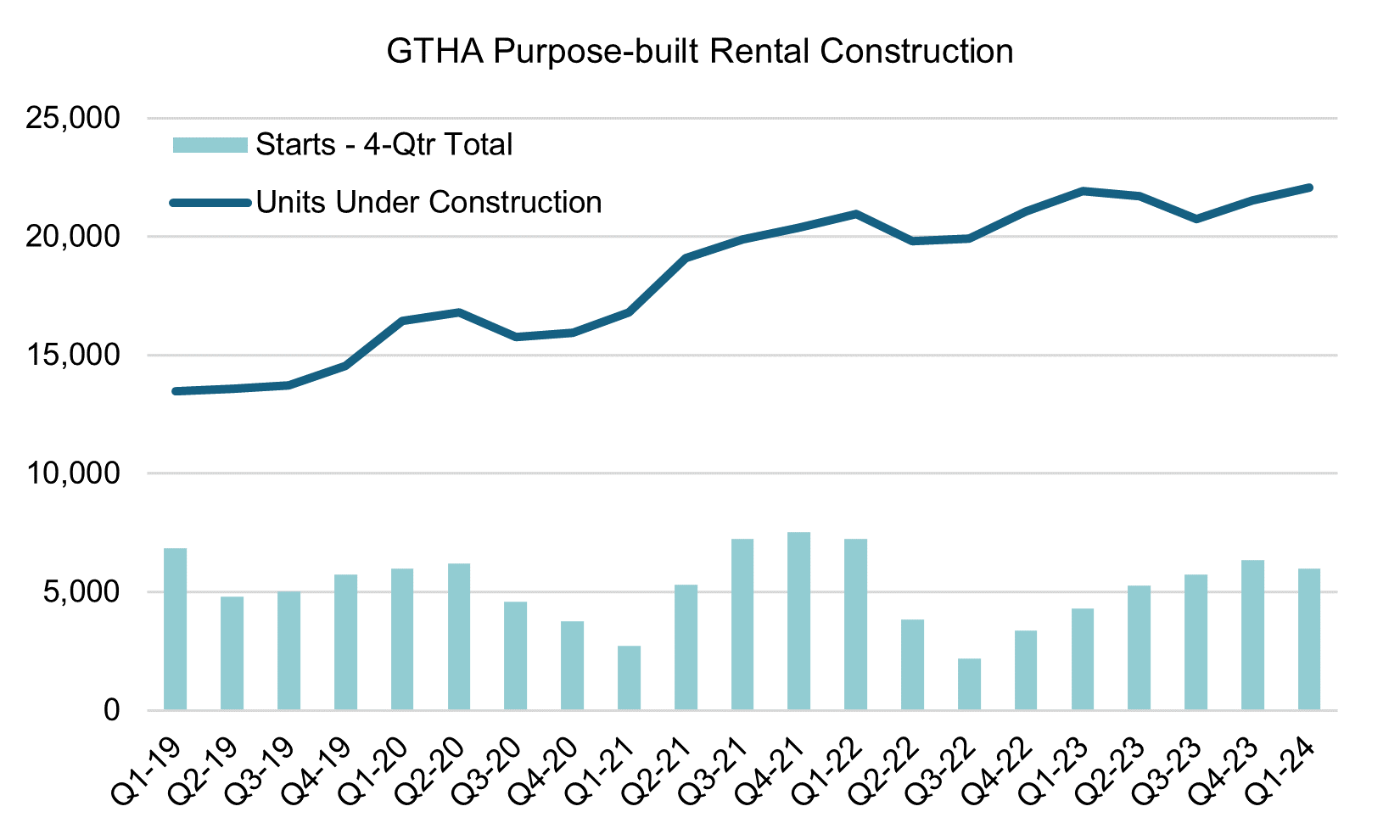

- Rental construction starts over past 12 months were up 174% from 2022 lows

After reaching a record high of $4.20 psf ($2,929 for 698 sf) in Q3-2023, average condo rents in the GTHA have declined 7.4%, the largest six-month decrease recorded during the past 15 years of data tracking outside of the pandemic period in late 2020/early 2021.

Despite this decline, average condo rents in the Greater Toronto Hamilton Area (GTHA) increased 1.6% year-over-year in Q1-2024 to $3.89 per square foot ($2,732 for 702 sf). Outside of the rent declines experienced during COVID-19, this represented the slowest annual pace of rent growth in nine years and a substantial deceleration compared to the 13.3% annual increase recorded a year ago in Q1-2023.

Supply from newly completed condos made a significant impact on the rental market. Over the past four quarters, a total of 23,095 new condos were registered, a 21% increase over the same period ending Q1-2023 (19,028) and the third highest four-quarter total ever recorded. Additionally, a record high 12,132 new condo units began occupancy in Q1 alone, adding further ‘shadow’ rental supply to the market.

Buildings registered in the past four quarters represented a record 24% share of all condos listed for rent in Q1-2024. Overall, the 37% year-over-year increase in condo rental listings more than doubled the 15% increase in leases signed during Q1-2024. This pushed active condo rental listings at quarter-end up to 5,078 units — a 55% quarter-over-quarter increase and more than double the level from Q1-2023 (2,516).

For purpose-built rental buildings completed since 2003, rents increased 2.0% quarter-over-quarter and 4.5% year-over-year to an average of $4.14 psf ($2,933 for 723 sf). The continued growth in rents for purpose-built rentals came as new supply slowed. After reaching a multi-decade high of 5,779 units for the year ending 2023, purpose-built rental completions fell to a six-quarter low of 783 units in Q1.

The 2.6% vacancy rate for purpose-built rentals in Q1-2024 represented a slight increase from Q4-2023 (2.5%) and a modest increase compared to a year ago in Q1-2023 (2.0%), but still representative of an undersupplied market. Vacancy rates were highest in non-rent controlled buildings completed since 2019 at an average of 3.5%, compared to pre-2019 rent-controlled buildings averaging vacancy of only 1.7%.

Since the government announced the removal of GST on new purpose-built rentals in November 2023, progress has been made towards improving construction activity. Over the last four quarters, a total of 5,976 purpose-built rental units started construction, a 174% increase off the low of 2,182 starts in the four-quarter period ending Q3-2022. However, the latest annual total for starts remained below the recent high of 7,540 starts recorded in 2021, and starts were down 21% year-over-year in Q1-2024 to 1,329 units. The total inventory of purpose-built rentals under construction in the GTHA reached a multi-decade high of 22,064 units in Q1-2024.

“While the market remains expensive with rents 15% higher than two years ago, renters waiting for some reprieve in the market have found it thanks to a temporary supply infusion from condo investors. This isn’t expected to last long, and rents should continue rising as construction falls short of demand.”

Shaun Hildebrand, President of Urbanation.

Latest Research

May 4, 2026

Over Half of Ottawa Rental Buildings Offering IncentivesApril 26, 2026

GTHA Rental Vacancy Rises to 5.4% in Q1April 16, 2026

Standing Condo Inventory Hits Record High in Q1February 9, 2026

GTA Land Transaction Volume Down 20% in 2025February 9, 2026

Rental Vacancy in Ottawa Increased to 3.5% in Q4January 29, 2026

Nearly 10,000 GTHA Rentals Started Contruction in 2025

In The News

April 30, 2026

Incentive offers rise as apartment operators compete with condos for tenantsApril 28, 2026

The vacancy rate is up for new Toronto area rental buildings, so why is it still so expensive to rent?April 21, 2026

Toronto's condo market 'hits bottom' with some developers looking at selling units below the cost to buildApril 17, 2026

'Somewhere to put worker bees': Why Canada's micro-condos are losing their appealApril 17, 2026

Toronto’s condo market sets a new record: zero new projects launched in the first quarterApril 10, 2026

Average national asking rents fall to $2,008 after largest drop in five years: report