TORONTO – April 22, 2024: Urbanation Inc., the leading source of information and analysis on the condominium market since 1981, released its Q1-2024 Condominium Market Survey results today.

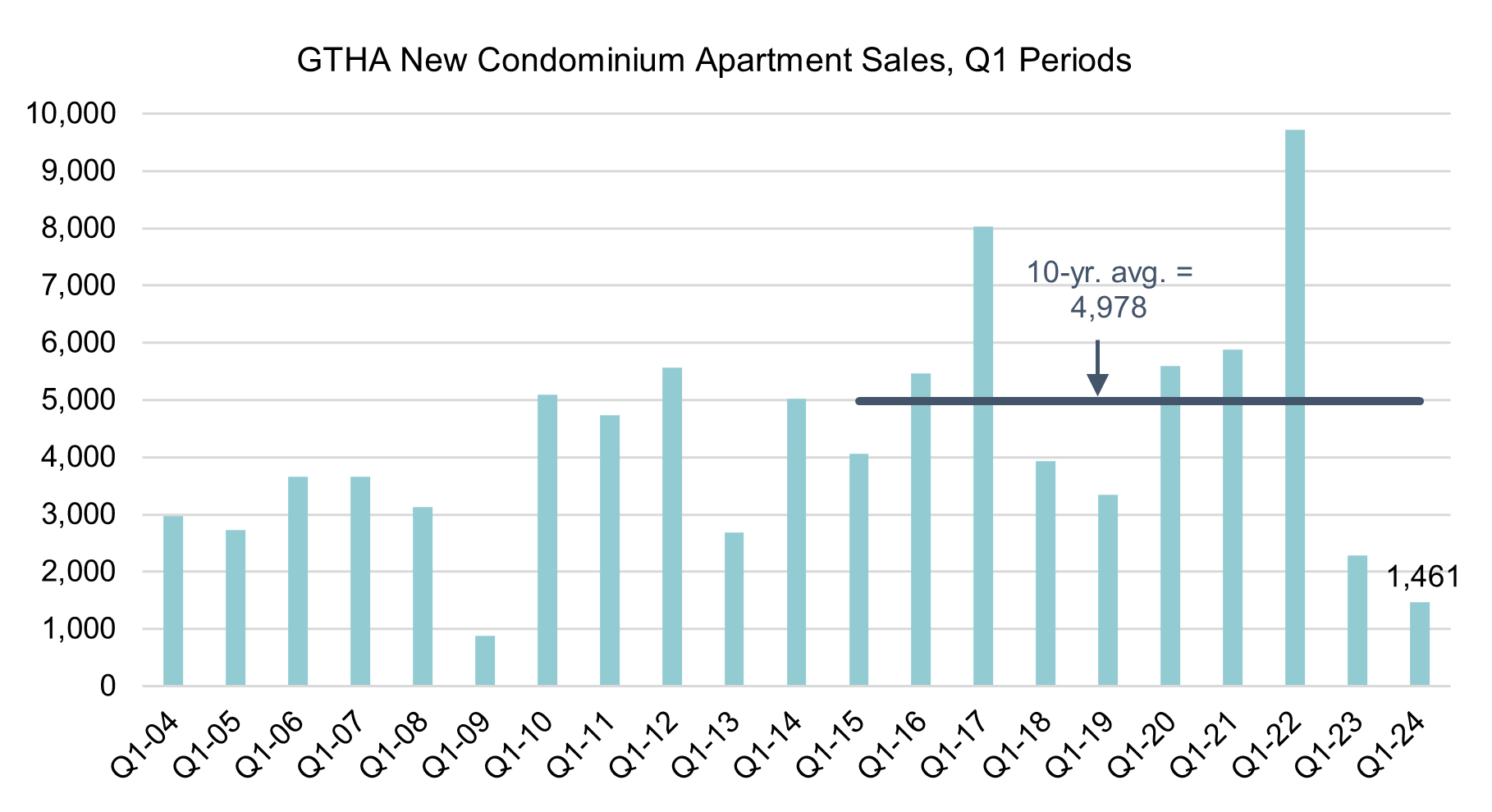

The Greater Toronto Hamilton Area (GTHA) new condominium market reported 1,461 sales in Q1-2024, the lowest quarterly total since the Global Financial Crisis in Q1-2009 (884 sales). Outside of that brief period in early 2009, new condominium sales haven’t been this low since the late-1990s. Sales were down 71% when compared to the latest 10-year average for Q1 periods (4,978 sales), dropping 85% from the Q1 high in 2022 (9,723 sales).

Developers dramatically pulled back on new launches in early 2024, with only four projects totaling 958 units brought to market in the first quarter. Three out of the four projects launched in the GTHA during Q1 were in the 905 Region, resulting in an average opening price for new condos of $1,168 psf — down 12% from Q4-2023 ($1,333 psf) and a 17% drop from the record high in Q1-2023 ($1,407).

Unsold inventory across all stages of development dipped 2% quarterly from the record high in Q4-2023 to 23,815 units in Q1-2024, equal to a high of 22.8 months of supply. In the past year, unsold new condominium supply increased 30%, rising 124% over the past two years.

As of Q1-2024, the City of Toronto (416 Region) had unsold new condo inventory equal to 30.6 months of supply. In the 905 Region of the GTHA, supply was equal to 16.8 months. Asking prices for unsold units in the 905 Region continued to edge higher in Q1-2024, rising 2% annually to an average of $1,161 psf. Meanwhile, prices for remaining inventory in the 416 Region decreased 4% year-over-year to an average of $1,522 psf. Overall, asking prices for unsold units in the GTHA declined 3% annually to an average of $1,373 psf. Additionally, there was widespread use of incentives, among which included reduced or free parking, reduced or no development levies, reduced deposits of less than 15%, rental guarantees, 5% or higher broker commissions, interest on deposits and mortgage assistance programs.

On average, projects in pre-construction during Q1-2024 were 50% presold, down from a 61% average absorption level a year ago and 85% two years earlier. With pre-construction sales falling well below typical construction financing requirements of at least 70% absorption, construction starts have experienced a sharp decline. In Q1-2024, 2,361 new condominiums began construction in the GTHA, down 52% annually. At the same time, completions surged to a record high of 12,132 units in Q1-2024, causing the total number of condos under construction to fall to a more than two-year low 91,590 units.

A total of 17,076 units across 56 projects have released marketing materials for an upcoming launch in the next couple quarters, with a 70% share of units located in the 905. Since the market began slowing in 2022, Urbanation has counted 60 projects to date totaling 21,505 units in the GTHA that were slated for launch and began releasing promotional material but have put their plans on hold indefinitely.

“The market for new condominiums started 2024 where it ended off in 2023, very slow. After two years of preconstruction sales trending down sharply, construction activity is being hit hard. While anticipated reductions in interest rates in the second half of the year should lead to some improvement in market conditions for new condominiums, activity will likely remain subdued as the industry works it way through current inventory and digests the numerous government policies on housing recently released.

--Shaun Hildebrand, President of Urbanation

Latest Research

July 27, 2026

GTHA RENTAL MARKET SHOWS IMPROVEMENT IN Q2July 20, 2026

GTHA NEW CONDO SALES INCREASE OVER 50% IN Q2June 23, 2026

Ontario Student Housing Deliveries Set to Reach Record in 2026May 4, 2026

Over Half of Ottawa Rental Buildings Offering IncentivesApril 26, 2026

GTHA Rental Vacancy Rises to 5.4% in Q1April 16, 2026

Standing Condo Inventory Hits Record High in Q1

In The News

July 28, 2026

GTHA rental market shows improvement in Q2July 21, 2026

Bulk investor buying helps resuscitate condo purchases in the Toronto regionJuly 21, 2026

New condo sales in the GTHA were up for the first time in 3 years, but report says supply now ‘thinning quickly’April 30, 2026

Incentive offers rise as apartment operators compete with condos for tenantsApril 28, 2026

The vacancy rate is up for new Toronto area rental buildings, so why is it still so expensive to rent?April 21, 2026

Toronto's condo market 'hits bottom' with some developers looking at selling units below the cost to build