TORONTO – April 27, 2026: Urbanation Inc., the leading source of data and analysis on the Greater Toronto Hamilton Area (GTHA) condominium and rental apartment markets since 1981, released its Q1-2026 rental market results today.

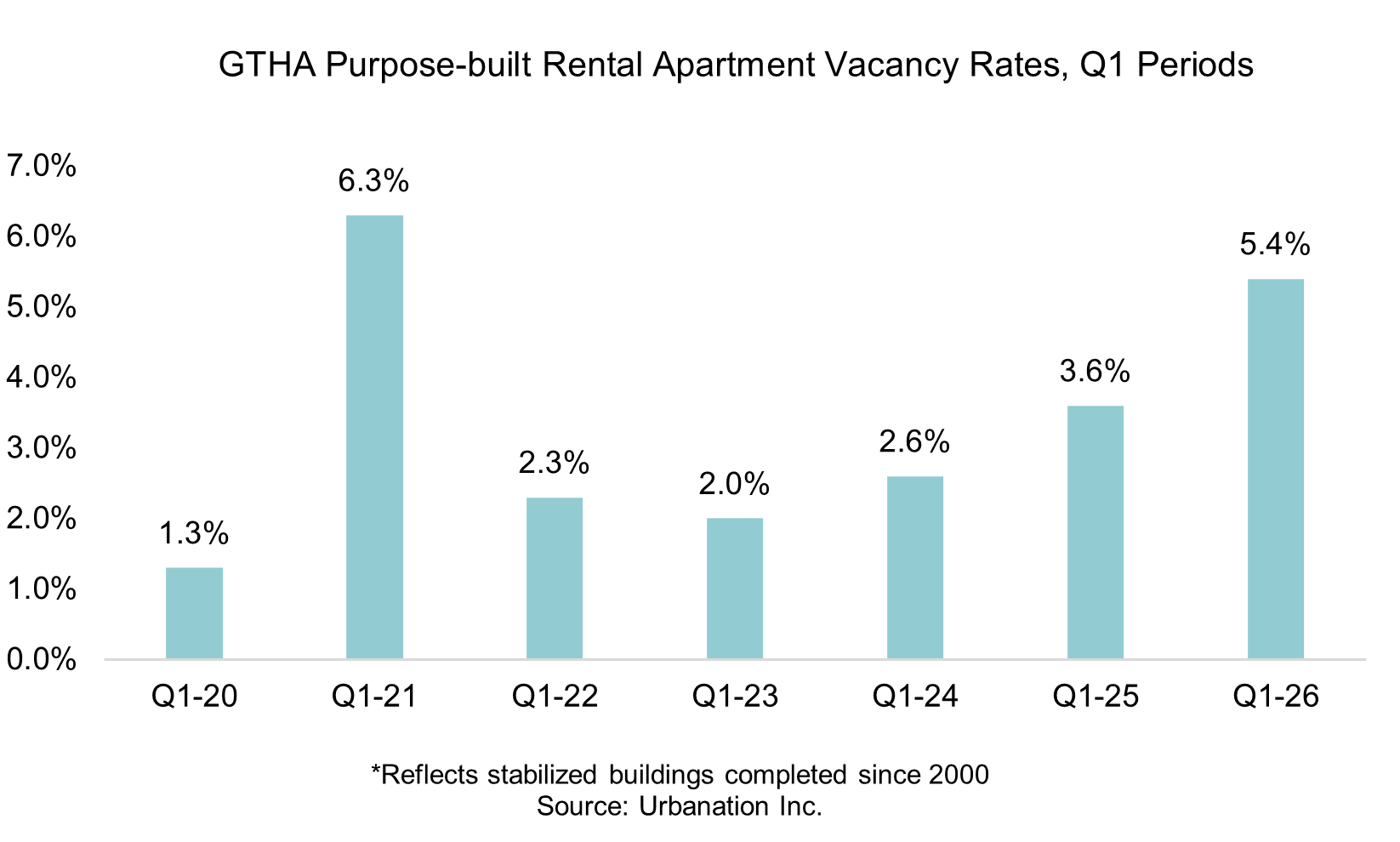

The vacancy rate in stabilized buildings completed since 2000 in GTHA was 5.4% in Q1-2026, rising from 3.6% a year ago in Q1-2025 and more than double the vacancy rate of 2.6% two years ago in Q1-2024. It was the highest vacancy rate seen since the pandemic in Q1-2021 when vacancy reached 6.3%. Vacancy increased as population inflows slowed and tenant turnover increased as renters took advantage of decreasing rents. The availability rate, which includes both vacant units and occupied units where the tenant has given notice to vacate, reached a record high of 8.0% in Q1.

Rental operators continued to heavily rely on incentives to attract tenants. In Q1, a 66% share of projects offered incentives, up from 62% a year ago and more than double the 32% share from two years ago. The most common incentive in the latest quarter was two months of free rent, offered at 47% of projects and rising from a 32% share last year. At the same time, the share of projects offering one month of free rent decreased to 42% from 53% a year ago. Cash move-in bonuses became more common over the past year, rising from 10% to 17% of projects, as did 1.5 months’ free rent (from 2% to 6%) and three months’ free rent (from 1% to 4%).

After accounting for the monetary value of incentives offered in the market, net rents in Q1 averaged $3.52 psf — down 3.8% annually to a 16-quarter low. Incentives reduced “face rents” by an average of 13% or $379 (from $2,904 to $2,525). This brought purpose-built rents in line with condo rents averaging $2,543 in Q1.

Softening rents and rising vacancy didn’t stop developers from continuing to forge ahead with new purpose-built projects. A total of 3,674 units started construction in Q1, up 12% from last year. This followed 4,069 units that started in Q4-2025, raising the latest 12-month total for starts to a multi-decade high of 10,388 units. While completions in Q1 declined 61% from a year ago to an eight-quarter low of 915 units, the slowdown in supply is temporary as many projects pushed their occupancy dates into the coming quarters. In Q2 alone, 17 projects and 3,261 units are scheduled for occupancy, with a record-high of 8,984 units projected for delivery in the next 12 months.

“Rental operators are grappling with a deluge of supply at the moment due to intense competition from the condo market and a surge in tenants moving to get a better deal. Supply pressures will persist this year as apartment completions run high and population growth slows, creating a window of opportunity for renters to capitalize on improved affordability.

Shaun Hildebrand, President of Urbanation

Subscription Information: https://www.urbanation.ca/membership

Latest Research

July 20, 2026

GTHA NEW CONDO SALES INCREASE OVER 50% IN Q2June 23, 2026

Ontario Student Housing Deliveries Set to Reach Record in 2026May 4, 2026

Over Half of Ottawa Rental Buildings Offering IncentivesApril 26, 2026

GTHA Rental Vacancy Rises to 5.4% in Q1April 16, 2026

Standing Condo Inventory Hits Record High in Q1February 9, 2026

GTA Land Transaction Volume Down 20% in 2025

In The News

July 21, 2026

Bulk investor buying helps resuscitate condo purchases in the Toronto regionJuly 21, 2026

New condo sales in the GTHA were up for the first time in 3 years, but report says supply now ‘thinning quickly’April 30, 2026

Incentive offers rise as apartment operators compete with condos for tenantsApril 28, 2026

The vacancy rate is up for new Toronto area rental buildings, so why is it still so expensive to rent?April 21, 2026

Toronto's condo market 'hits bottom' with some developers looking at selling units below the cost to buildApril 17, 2026

'Somewhere to put worker bees': Why Canada's micro-condos are losing their appeal